En

EnFreight forwarder DSV reported 3Q revenues that were 9% higher than a year earlier, and beat analysts’ expectations. An 8% growth in volumes was twinned with achieved rates that were broadly unchanged. That allowed it to outperform peers K+N and Panalpina that saw falling profit margins after more aggressive volume expansion. DSV’s profitability (earnings before interest, tax, depreciation and amortization vs. revenues) was better than expected at 8.0% vs. 7.0% a year earlier due to extensive cost cutting after the UTi acquisition. While DSV may not outperform the sector’s expected reven...

Supply Chain Research

Related Research

Supply Chain Edge: Building on the ‘70s, delaying tariffs, shipping slips

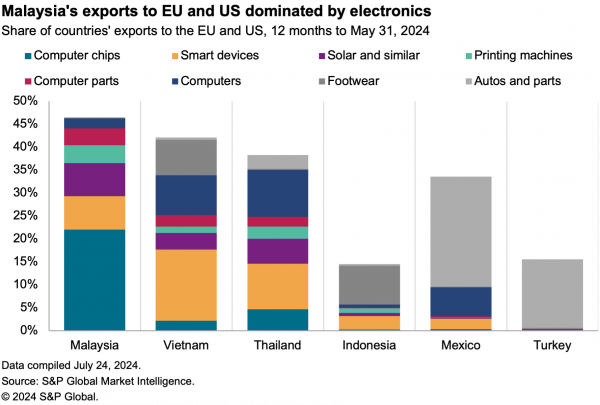

– In new research this week, we look at Malaysia’s future as a reshoring center, which has been building since the 1970s but now ... Read more →

Supply Chain Edge: Olympian sourcing, Mexican metals, expensive memories

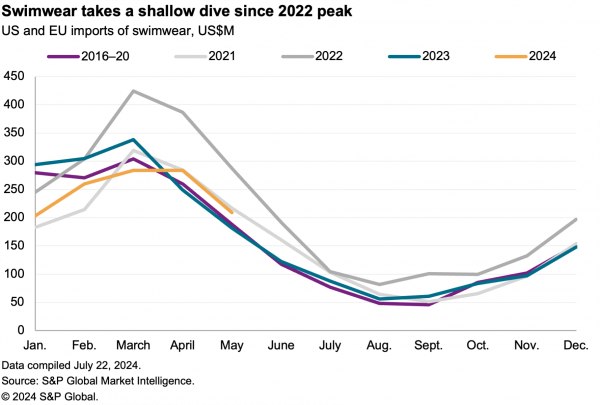

– The Paris 2024 Olympic and Paralympic Games present an opportunity to revive the declining sports equipment and apparel supply ... Read more →

Supply Chain Edge: Under the EU influence, spinning up electronics

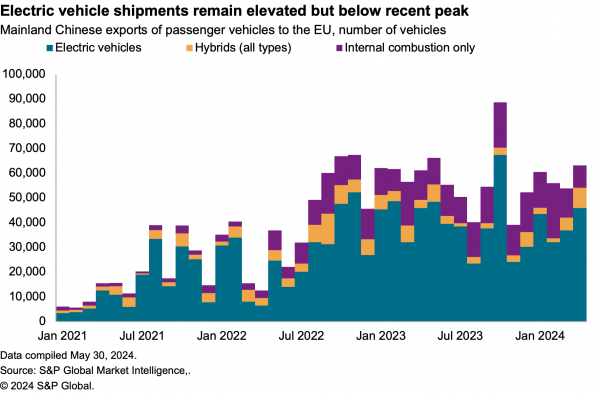

• The EU may delay its initial judgment on mainland China’s electric vehicle supply chains, reducing geopolitical pressures, alth... Read more →

Supply China Edge: Tech restrictions widen, Adidas kicks inventory, rate boom returns

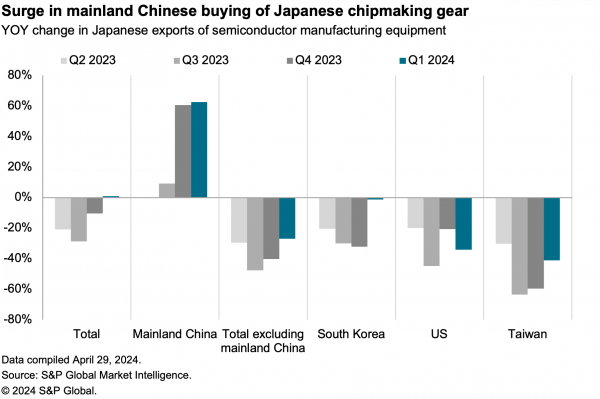

• In new research this week, we dive into Japan’s latest technology restrictions, which follow a surge in exports to mainland Chi... Read more →

Copyright © 2024 Panjiva Supply Chain Intelligence, a product offering from S&P Global Market Intelligence Inc. All rights reserved.