En

EnThe U.S. Commerce Department has “self initiated” anti-dumping and countervailing subsidy cases against Chinese aluminum sheet exports, marking the first time since 1991 that such a strategy has been followed.

The timing is curious given that the administration is currently working on an (effectively self-initiated) section 232 review of the entire aluminum industry. That has been delayed, along with a matching steel case, due to the ongoing tax reform process as outlined in Panjiva research of November 21. It’s probably too early to say, however, that this latest move reflects an expectation that the section 232 review will lack any “interesting” outcomes.

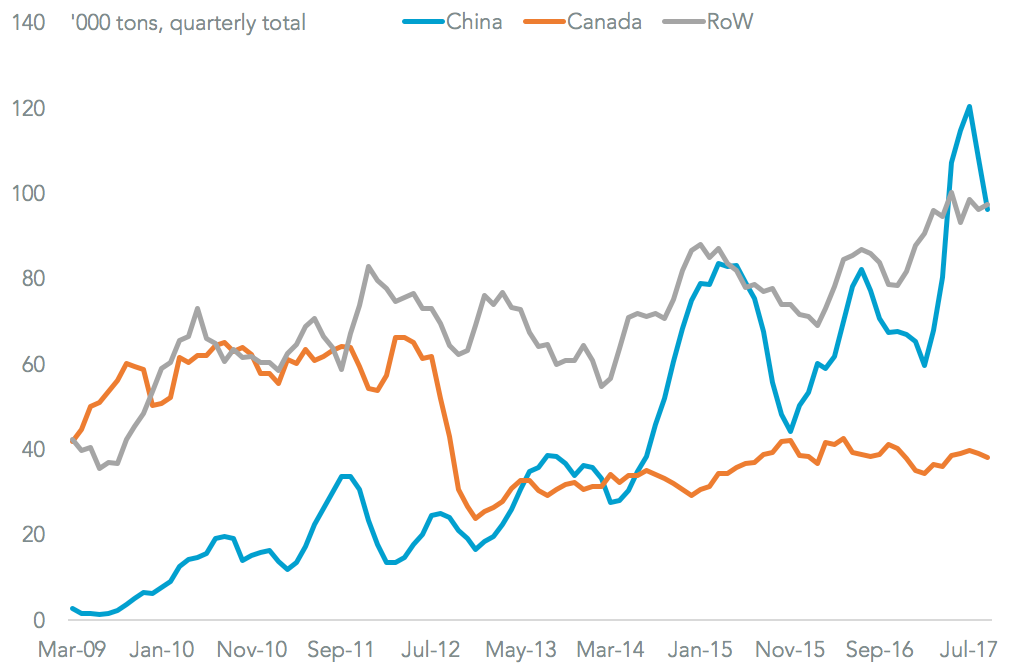

From a targeting perspective the case makes sense. Panjiva data shows that total U.S. imports climbed 18.5% on a year earlier in the 12 months to September 30 in volume terms, and by 16.6% annually for the past three years. Chinese exports to the U.S. climbed 33.9% in the past year. The main losers have been Canadian exporters. However, the peak may already be past, with Chinese exports in the third quarter having fallen 16.2% vs. the second.

Source: Panjiva

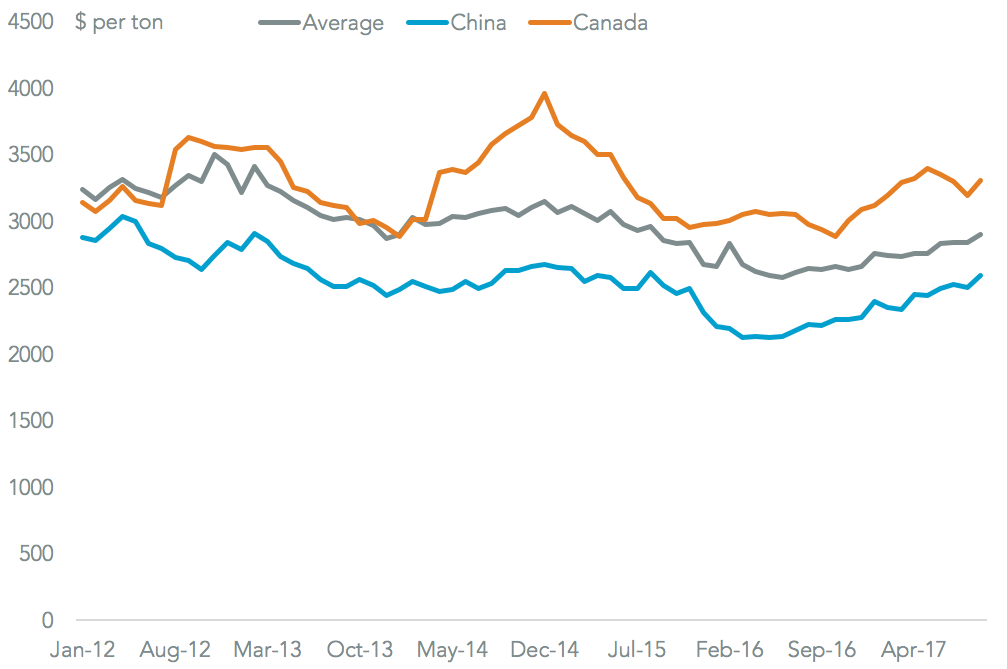

Notably can-stock has been excluded, possibly to avoid a significantly negative direct on consumers (higher soda and beer costs). Other buyers of the product won’t be as lucky. Commerce Secretary Wilbur Ross has made it clear that beneficiaries of “cheap steel” cannot expect to continue to receive it. On average the Chinese imports’ value per ton in the past year were 12.8% cheaper than that for all imports, and 24.9% cheaper than those from Canada (mix effects aside).

Source: Panjiva

Tariffs, or quotas, applied could be a significant issue for the Chinese manufacturers involved. The U.S. represented 19.0% of total Chinese exports of the broader sheet aluminum products involved over the past two years. Historically though diversions to other Asian markets – particularly Vietnam and India – has been a reaction from manufacturers.

Source: Panjiva